Best Retirement Calculator: Why One Number Is Not Enough

Understand what a retirement calculator should do and use a five-tool framework that turns each answer into your next retirement decision.

16 min read

Key Takeaways:

Most retirement portfolios are built to grow wealth. This one was built to distribute income and survive difficult markets.

The biggest risk in retirement is not just market losses. It’s needing to withdraw income while your portfolio is down. A portfolio can recover. But withdrawals during a major downturn permanently change the math.

The 4% rule says you can withdraw 4% of your portfolio annually with a high probability of not running out of money over a 30-year horizon. That research is legitimate, but it’s incomplete.

For investors who need more, and many do, the standard playbook runs out of options quickly. High-yield bonds add credit risk. Dividend stocks concentrate equity risk. Annuities sacrifice flexibility and hide massive fees. None of these solve the underlying problem, which isn’t the yield. It’s the single source producing it.

Berkshire Hathaway works because it owns many different kinds of businesses. Railroads, insurance, utilities, and consumer brands do not all struggle at the same time. Retirement income should work the same way.

Most income portfolios rely on one engine: dividends, bonds, or market appreciation. This portfolio was built differently, using multiple independent sources of income designed to behave differently in different markets. The diversification isn’t in the names. It’s in the profit engines.

That is the blueprint for a sustainable income portfolio.

Reaching retirement is an accumulation problem. Staying there is a structural one. This portfolio is built for the second problem.

Several years ago, I was in a client meeting discussing their retirement income needs. The markets looked a lot like today, filled with bad headlines and uncertainty. Suddenly, the client burst out:

This is all the money I have. I cannot afford to lose it. But I need more income than the 4% rule. I need 5% or more after the bank’s management fee.

The conversation with my client forced a different starting question: “How can I deliver a portfolio that avoids catastrophic losses?”

Most investors simply chase yield when they need more income. But this often leads to riskier stocks or bonds. That doesn’t solve the problem; it just moves the risk somewhere less visible.

The answer drove every allocation decision. And it led directly to the Berkshire framework, not because Berkshire holds exchange-traded funds (ETFs), which are baskets of investments that trade like stocks, but because Berkshire solved the same problem at a different scale. Diversify the business model, not just the balance sheet.

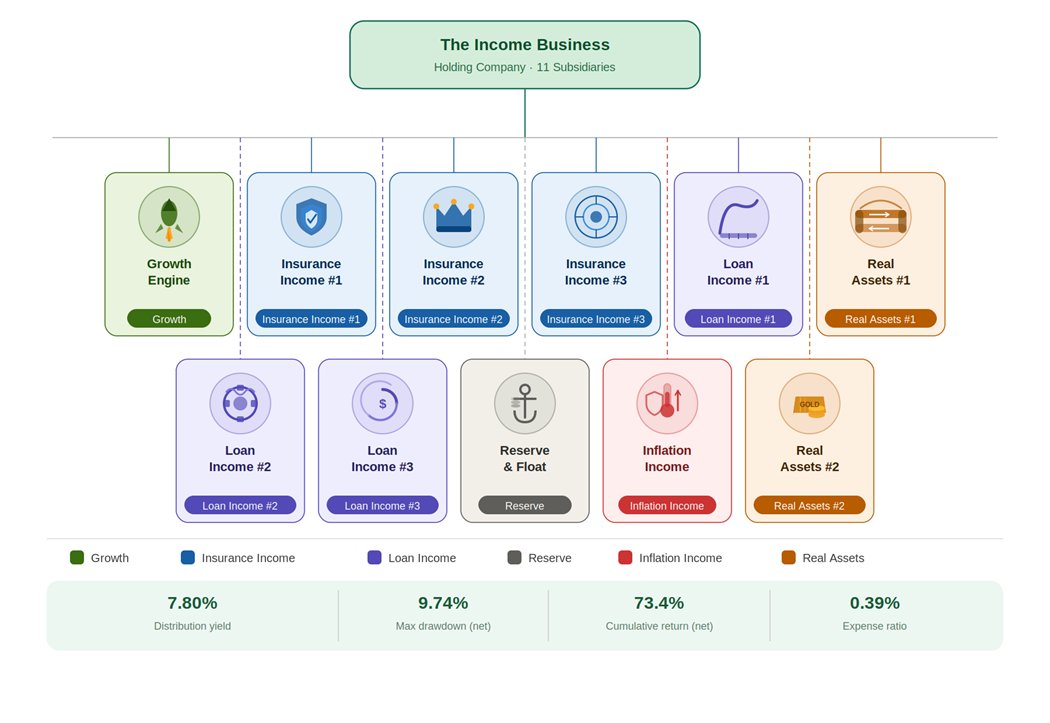

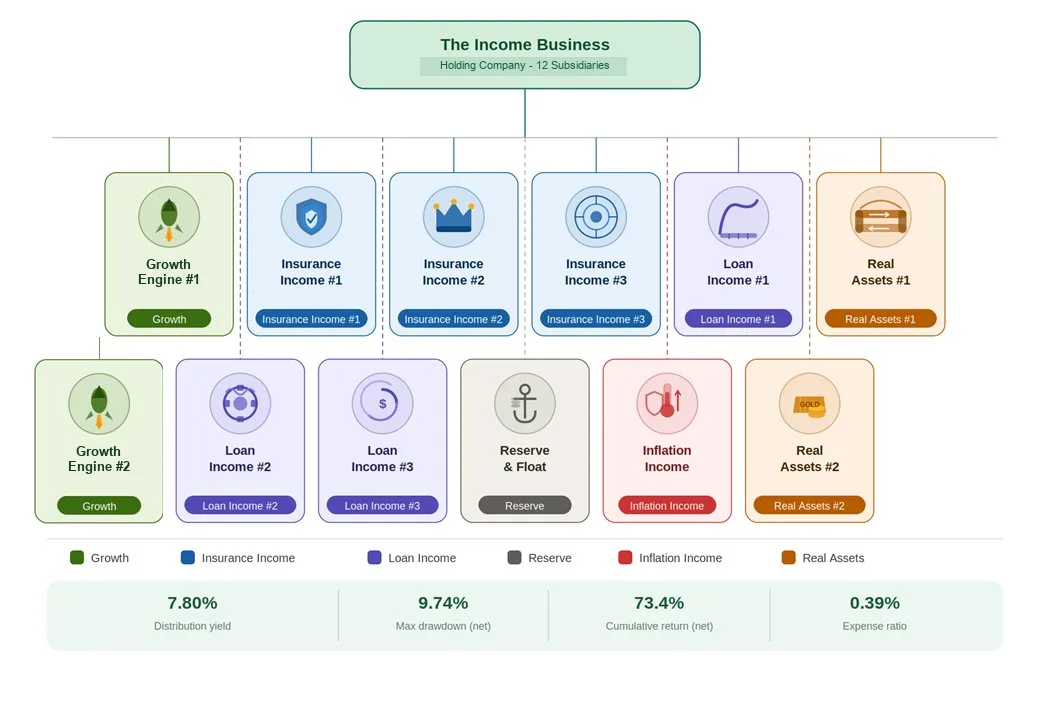

The diagram below shows how the portfolio is structured. Each card is a “subsidiary”: a distinct income-generating business with its own profit mechanism, color-coded by category. Gold+ subscribers receive the complete breakdown: every instrument named, weighted, and analyzed in full. The advanced tool also allows for complete customization to your specific income and risk needs.

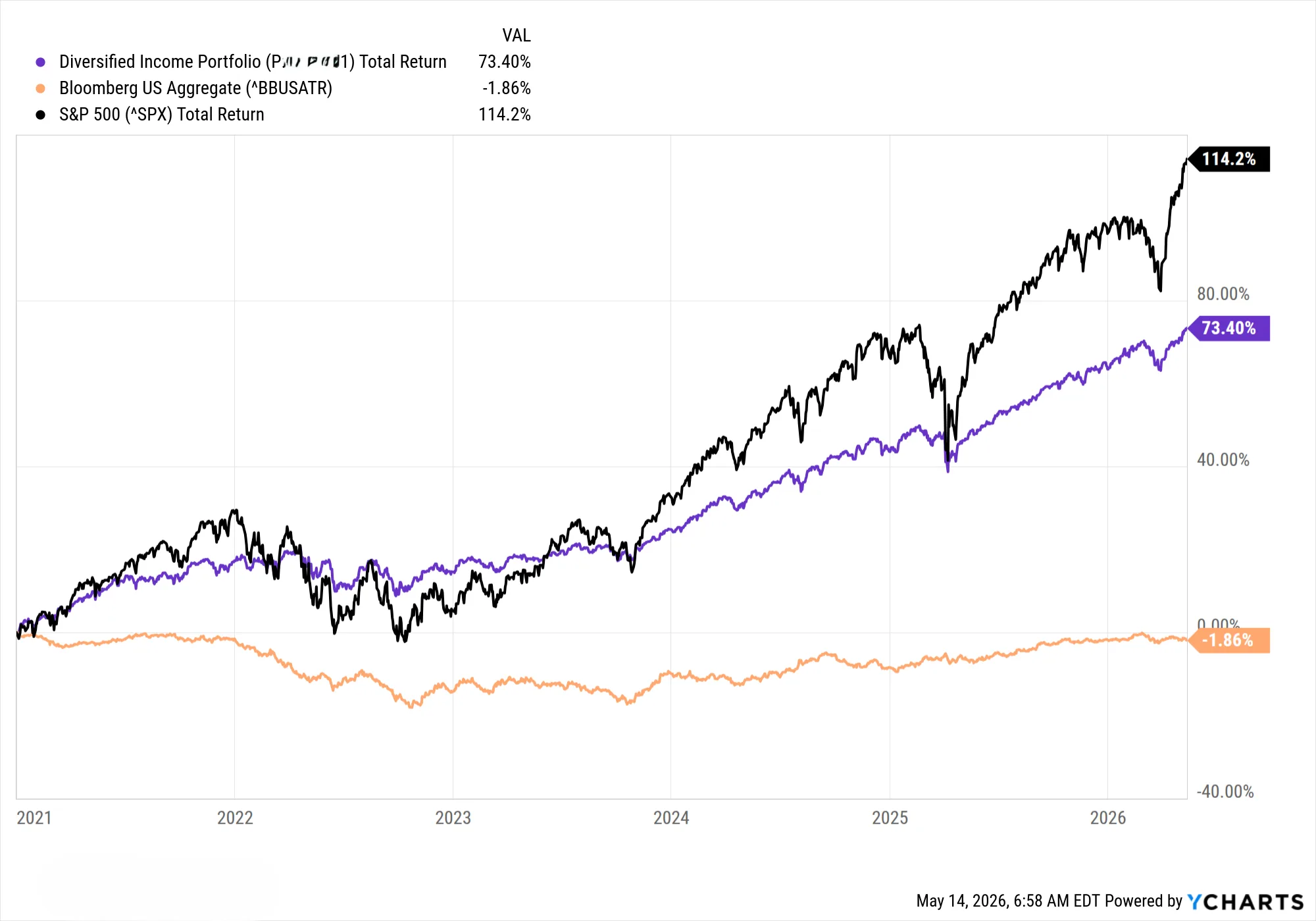

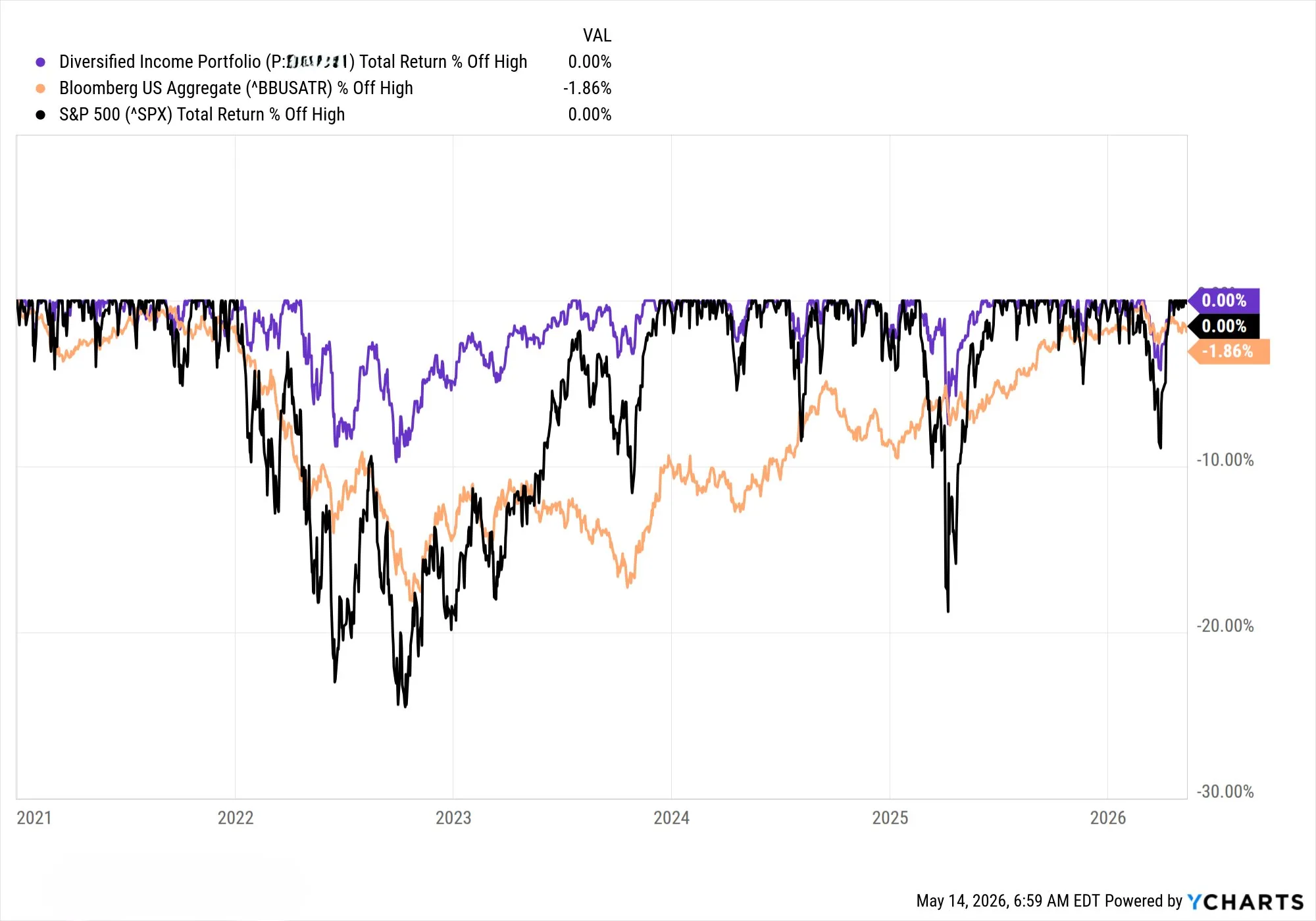

The portfolio generated more income with less downside than many traditional retirement portfolios. In 2022, when the Bloomberg US Bond Aggregate fell 13% and a traditional balanced portfolio of stocks and bonds was down more than 20%, this portfolio lost less than 10%.

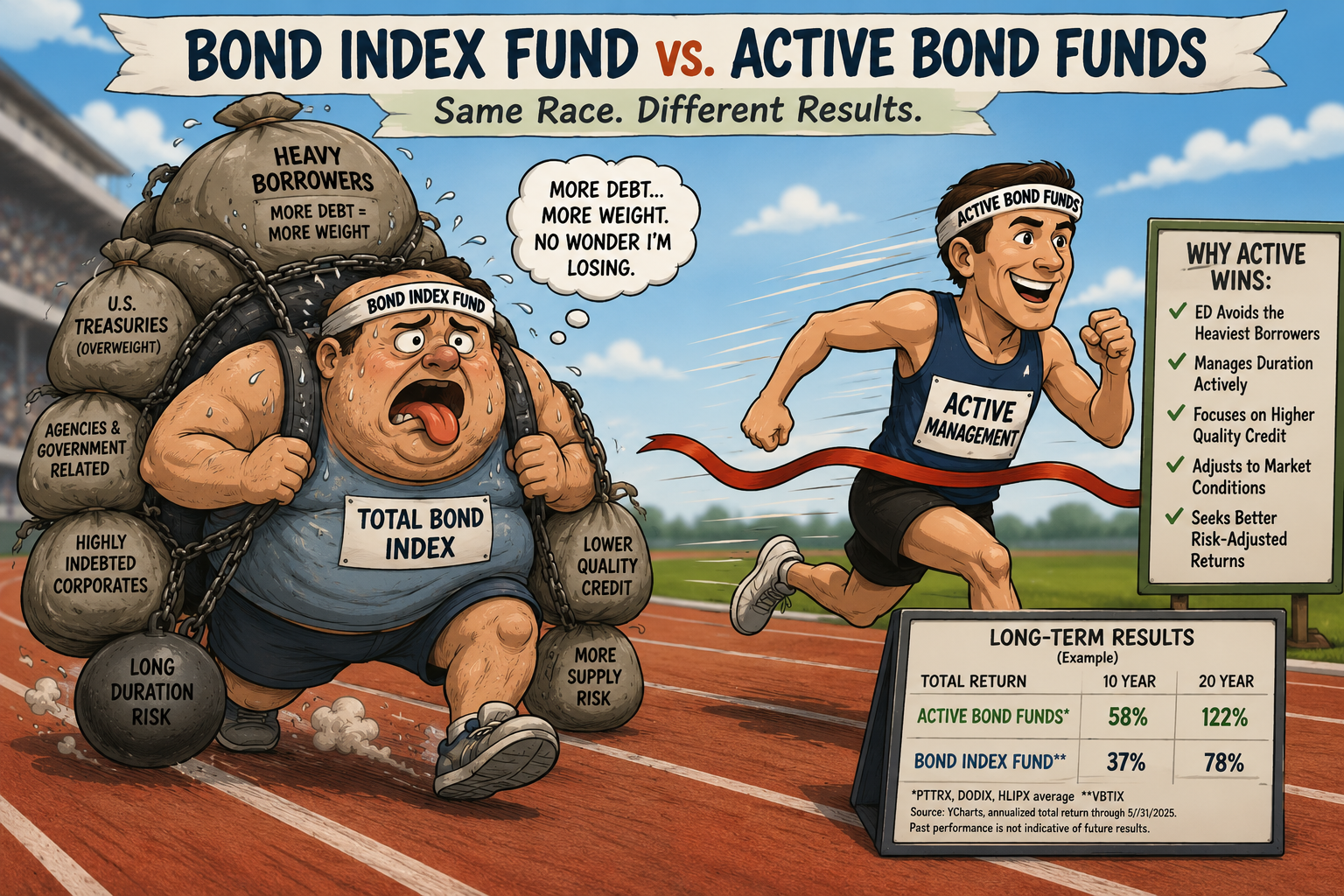

This is also why I do not treat total bond funds as automatically safe. The way bond indexes are built can work against retirees, which is the problem I covered in how to choose bond funds for retirement.

| 7.80% Distribution yield | 0.39% Underlying expense ratio | 9.74% Max drawdown | 7.20% Additional return |

After fees, the portfolio delivers income well above the 5% threshold it was designed to target, with a max drawdown less than half that of the Bloomberg US Aggregate over the same period.

The income is not driven by taking extreme risk or speculative leverage. It comes from combining multiple complementary income strategies designed to behave differently across market environments.

This portfolio was not designed to beat the S&P 500. It was designed for an investor who cannot afford to lose principal and needs 5%+ in income. Those are not the same objective, and the charts below reflect that directly.

From inception through May 2026, the portfolio returned 73.40% cumulatively. The S&P 500 returned 114.2% over the same period. That gap is the cost of the income mandate and the capital preservation requirement. It is not a failure. It is the price of sleeping at night.

When markets are stressed, the tradeoff reverses sharply in the portfolio’s favor. The drawdown chart is where the holding company structure earns its keep.

Two-thirds the cumulative return of the S&P 500, with 7.80% annual income and a fraction of the downside. That is not a consolation prize. It is a different product solving a different problem.

Every time the S&P 500 fell 20%+ from its highs, this diversified portfolio held its shape. The worst drawdown was 9.74%, less than half the market’s peak-to-trough loss. For a retiree needing 5%+ annually, the difference between a 10% drawdown and a 25% drawdown is not academic. It is the difference between a recoverable sequence-of-returns event and a portfolio that never comes back.

The actual value proposition: not “beat the market,” but “stay in the game long enough for the income to compound.”

I’ve spent years managing money for families who cannot afford catastrophic mistakes in retirement. Building wealth and living off your wealth are different problems.

Most portfolios are designed for accumulation. Very few are designed for sustainable retirement income through difficult markets.

Nobody is watching your retirement income.

Gold+ is your retirement navigation system: find your number, follow the Harbor or Sustain Portfolio matched to your withdrawal rate, and get a specific action when market risk changes.

This article is for educational and informational purposes only and does not constitute investment advice. If this article discusses any security, the discussion is for educational purposes only and should not be interpreted as a recommendation, solicitation, or personalized advice. The author may have holdings in the securities discussed. Refined FI is NOT a registered investment advisor. Past performance is not indicative of future results. All investing involves risk, including possible loss of principal. All figures reflect the period from December 1, 2020 through May 14, 2026, sourced from YCharts. All return and drawdown figures are net of fees. Current distribution yield of 7.80% reflects trailing 12-month distributions, as of May 14, 2026, and is not a guarantee of future income. Refined FI receives $0 in affiliate revenue, commissions, or compensation from any fund company or financial institution mentioned in this article.

Understand what a retirement calculator should do and use a five-tool framework that turns each answer into your next retirement decision.

16 min read

BlackRock's BDVIX owns thousands of bonds, but retirement income diversification requires more than one income engine.

8 min read

The best bond funds for retirement are usually active, flexible funds, not debt-weighted indexes. Refined FI weighs inflation and stock-bond correlation first.

11 min read