Best Retirement Calculator: Why One Number Is Not Enough

Understand what a retirement calculator should do and use a five-tool framework that turns each answer into your next retirement decision.

16 min read

Key Takeaways:

People searching for the best bond funds for retirement usually want a list. I think that starts in the wrong place.

For retirees, the better answer is usually an active bond fund category, not a debt-weighted index fund. But Refined FI still would not recommend a fund by name until the broader portfolio map accounts for inflation, interest rates, and whether stocks and bonds are moving together.

For years, investors have been told to index everything. Buy the market. Keep costs low. Do not pay someone to guess. Let compounding do the work.

For stocks, that advice is usually more right than wrong. Most active stock managers struggle to beat their benchmarks over long periods. A broad, low-cost stock index gives you exposure to the companies that have earned a larger place in the market.

But bonds work differently.

The logic that makes indexing powerful in stocks does not transfer cleanly to fixed income. The mechanics are different. The incentives are different. And the long-term results tell the real story.

If you have carried your stock-indexing philosophy into your bond allocation without looking under the hood, you may have quietly added risk to your portfolio while accepting lower long-term returns.

Especially in retirement.

Because the bond sleeve is usually supposed to be the stable part of the portfolio. The ballast. The income source. The piece that helps you avoid selling stocks at the wrong time.

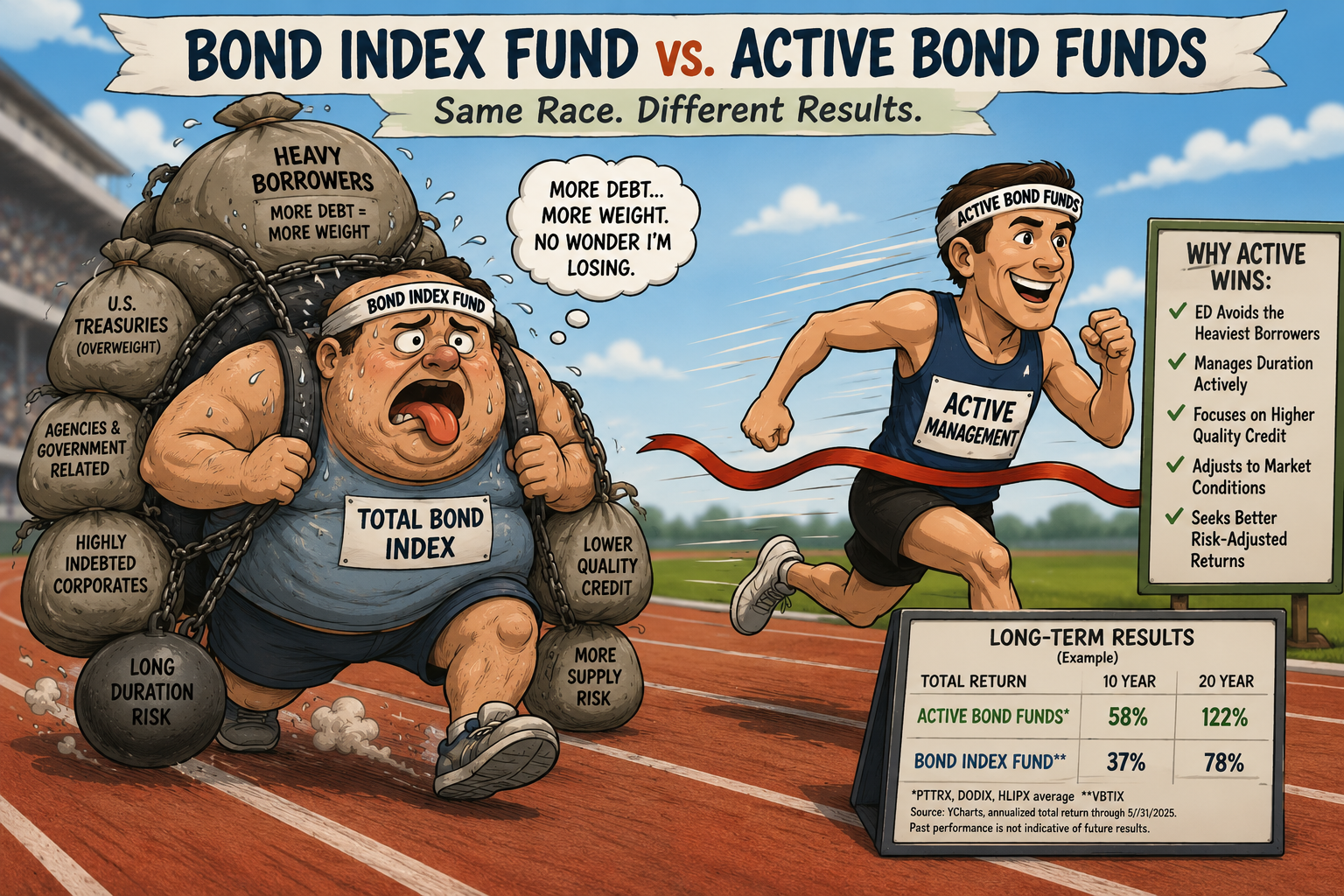

But a total bond index has a structural flaw most investors are never taught. It allocates the most money to the borrowers who have the most debt.

Imagine a footrace where the heavier a runner gets, the more money you are required to bet on them.

Not because they are faster. Not because they are healthier. Not because they have trained more than everyone else. Simply because they gained more weight.

That is close to how a total bond index works.

The most widely followed bond benchmark is the Bloomberg U.S. Aggregate Bond Index, often called the Agg. It is the benchmark behind many total bond market funds, including Vanguard’s VBTIX, BND, AGG and similar funds from other major providers.

The Agg is weighted by the market value of debt outstanding. In plain English: the more debt an issuer has, the bigger its share of the index.

That means the U.S. government is the largest piece of the index largely because it has borrowed more than anyone else. As federal debt grows, the government’s weight in your “diversified” bond fund grows with it.

The same logic applies to corporations. A company with $10 billion of bonds outstanding gets roughly twice the index weight of a company with $5 billion outstanding, regardless of which company has the stronger balance sheet.

That is the strange part.

In stocks, size often reflects success. In bonds, size often reflects leverage and risk.

A stock index is usually weighted by market capitalization. If a company’s stock price rises, its market value rises, and the index owns more of it.

That is not perfect. Markets can get carried away. Valuations can become stretched. Concentration can build.

But the basic direction makes sense. Companies that create more value become larger parts of the index.

Bond indexing works in the opposite direction.

Stock Index vs. Bond Index

Stock Index

A company earns a larger place in the index as its market value grows. Size is a sign of business success.

Bond Index

A borrower earns a larger place in the index as it issues more debt. Size can be a sign of leverage and risk.

That is why stock indexing and bond indexing are not remotely the same.

A bond index does not give more weight to the most profitable borrower. It does not give more weight to the most disciplined balance sheet. It does not give more weight to the issuer with the safest margin of error.

It gives more weight to the issuer that has the most debt, period.

That is the core problem. Your total bond fund may look safe because it is diversified. But the weighting system quietly adds credit concentration risk to your portfolio.

Not capital to the best borrowers.

If this were only a theoretical problem, it would be easier to ignore. But the long-term numbers make the issue harder to dismiss.

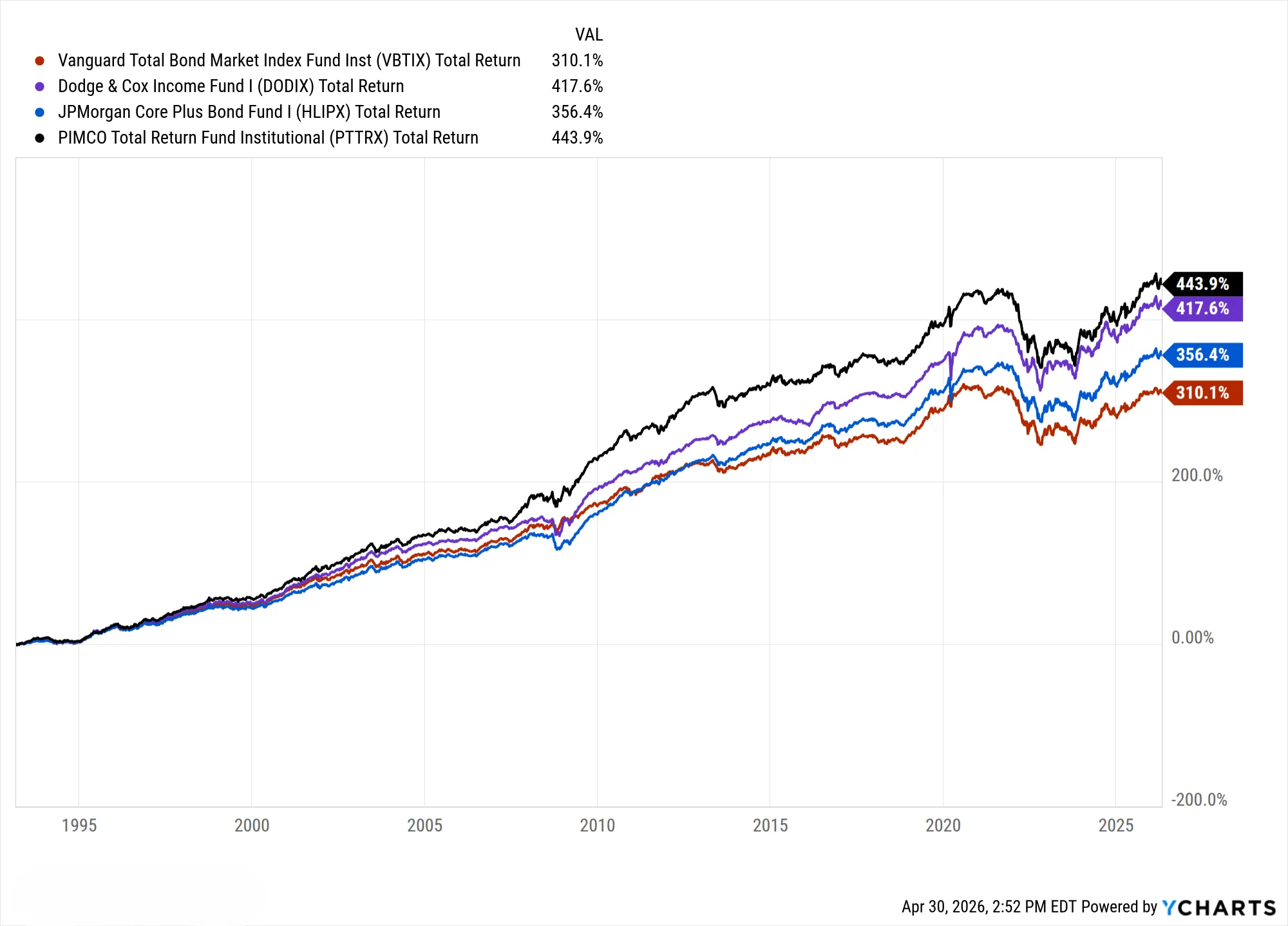

Over the 30-year period from 1994 through April 2026, several large actively managed bond funds meaningfully outperformed the broad bond index. The comparison in the original analysis used VBTIX, PTTRX, DODIX, and HLIPX.

The gap was not small.

PTTRX returned 443.9%. DODIX returned 417.6%. HLIPX returned 356.4%. VBTIX returned 310.1%.

What would your portfolio look like with an additional +130% of gains over 30 years?

This does not prove every active bond fund is better. It does not mean you should blindly replace every bond index with one of the funds listed above. They are examples, not blanket recommendations.

But it does suggest a structural difference: The bond market gives skilled managers more room to add value than many investors assume. That is very different from the stock market, where low-cost indexing has been brutally hard to beat.

The Ozempic analogy is intentional.

Ozempic works by suppressing appetite. It forces the body to stop eating past the point where more food helps. In short, it eliminates excess.

A good active bond manager does the same.

They are not forced to buy more of an issuer simply because that issuer has borrowed more money. They can say no. They can avoid the most bloated parts of the market. They can choose a different mix of duration, credit quality, sectors, and yield.

That flexibility matters for several reasons.

First, the bond market is materially less transparent than the stock market. There are thousands of issuers and hundreds of thousands of individual bond issues across Treasuries, agencies, mortgages, corporates, municipals, and structured credit. Many bonds trade over the counter instead of on a centralized exchange. Even many private companies issue debt.

Second, many bond market participants are not trying to maximize gains. They are investing in bonds to get a predictable yield and their investment back. Banks, insurance companies, pension funds, and regulated institutions often buy or sell bonds because their conservative rules require it. That can create opportunities for investors who are not forced to act at the same time.

Third, duration matters. A bond index does not ask whether interest-rate risk is attractive. It owns what the index owns. If the market has issued a large amount of long-duration debt, the index absorbs it.

That was painful in 2022.

The bond index’s heavy exposure to long-duration government debt made the rate shock especially damaging. Bonds were not the hedge investors expected that year. The stable part of the portfolio fell hard.

Active managers were not immune to the 2022 drawdown. But they had tools and flexibility that the index did not have.

They could shorten duration. They could adjust credit exposure. They could own inflation-protected bonds. They could avoid areas where investors are not being paid enough for the risk.

Active management creates room to make those decisions; an index cannot.

A bond index is mechanical. A good active bond fund can be selective.

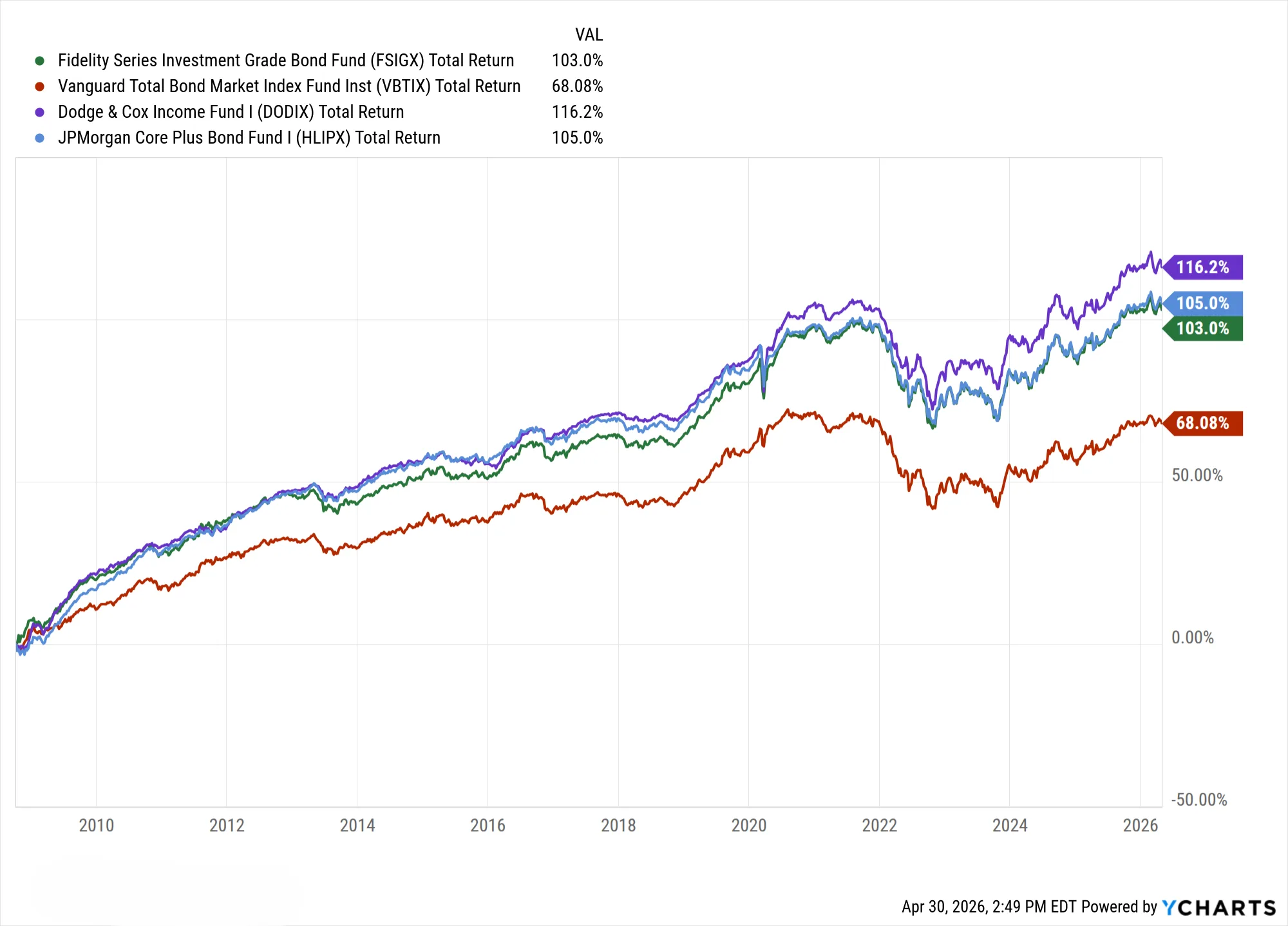

The more recent period tells the same story.

From 2009 through April 2026, the original analysis showed DODIX, HLIPX, and FSIGX ahead of VBTIX.

DODIX returned 116.2%. HLIPX returned 105.0%. FSIGX returned 103.0%. VBTIX returned 68.08%.

Again, this is not a guarantee that a specific active bond fund will win going forward.

It is evidence that bond indexing deserves more scrutiny than it usually gets.

The lowest expense ratio is not always the best value. Sometimes the hidden cost is assuming the index is automatically the best solution.

For a retiree, bonds are not decoration. They have a specific role to serve.

They may be there to generate income. They may be there to reduce volatility. They may be there to provide liquidity when stocks are down. They may be there to help avoid catastrophic sequence-of-returns mistakes.

If bonds are supposed to stabilize retirement income, the portfolio structure matters. That is why the retirement income portfolio is built around multiple income engines instead of a single bond index.

This is why I usually favor an active bond fund framework for retirement over a pure total bond index fund. No single active fund is always the answer. Your bond sleeve needs the flexibility to adjust when inflation, rates, credit spreads, and stock-bond correlations change.

For what that looks like in a specific fund, I put one through this exact test in my review of the BlackRock Diversified Fixed Income Fund.

That means the question is not, “Is indexing good or bad?”

Judge the fund by one standard: Does it actually do the job I need it to do?

A total bond index fund is not a meritocracy. It is an allocation machine weighted toward the largest debtors.

And that may have hidden risks to your portfolio, beyond lower returns.

The lesson is not that every active bond fund is a better investment. The lesson is that your bond allocation deserves more thought than “just buy the index.”

The safe part of your portfolio still needs underwriting.

Nobody is watching your bond fund, including the index it tracks.

Gold+ is your retirement navigation system: find your number, follow the portfolio built for your stage, and get a specific action when market risk changes.

This article is for educational and informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other sort of advice. Refined FI is not a registered investment advisor. Nothing in this article should be construed as a recommendation to buy, sell, or hold any security or financial instrument. Past performance of any index, fund, or investment strategy is not indicative of future results. All investing involves risk, including the possible loss of principal. The fund performance figures referenced are historical total returns and are subject to change. All figures are sourced from YCharts as of April 30, 2026, and reflect a specific point in time. Refined FI receives $0 in affiliate revenue, commissions, or compensation from any fund company, broker, or financial institution mentioned in this article. The views expressed are those of the author and do not represent any employer, client, or institution.

Understand what a retirement calculator should do and use a five-tool framework that turns each answer into your next retirement decision.

16 min read

BlackRock's BDVIX owns thousands of bonds, but retirement income diversification requires more than one income engine.

8 min read

The best bond funds for retirement are usually active, flexible funds, not debt-weighted indexes. Refined FI weighs inflation and stock-bond correlation first.

11 min read