Dead Weight: Zombies in Your Portfolio

If your portfolio holds small-cap funds, you're carrying dead weight into retirement. The market has changed.

6 min read

Key Takeaways:

For decades, investors were told to diversify. Own large-cap (large companies), mid-cap, and small-cap stocks, because those small companies will grow big one day.

That advice was built for a market structure that no longer exists.

Today high-growth companies increasingly stay private. What remains in public small-cap indexes is a growing concentration of unprofitable firms, serial diluters, and debt-dependent businesses.

Today, 42% of the Russell 2000 is unprofitable. If you own a total market index fund, you own them too.

Three pieces of legislation reshaped the economics of being a publicly traded company:

The cumulative effect was straightforward: being a public company became expensive, restrictive, and litigated. At the same time, private equity and late-stage venture capital became flush with capital. Companies that would have IPO’d in 1995 now stay private for a decade longer, sometimes forever.

The growth engine moved off-exchange.

The Russell 2000 used to be the proxy for the future of American business. Today, it tells a different story.

42% of all Russell 2000 constituents are currently unprofitable.

These are not lean, fast-growing firms about to break out. They are companies that survive by burning cash, diluting shareholders, and rolling over debt. The polite term in industry research is “zombie companies.” They aren’t growing into something. They’re a drag on your portfolio.

When you own a small-cap fund - or a total stock market index - you are wasting good capital.

The S&P 500 has a structural filter the small-cap index doesn’t: a company must show four consecutive quarters of positive GAAP earnings before it can enter the index. That filter eliminates the zombies by design.

The result is a performance gap that has widened over the past decade.

| Fund type | What it owns | Hidden issue |

|---|---|---|

| Total market index fund | Large, mid, and small companies | Includes unprofitable small caps |

| Small-cap fund | Smaller public companies | Higher zombie-company exposure |

| S&P 500 fund | Large profitable companies | Earnings screen removes many zombies |

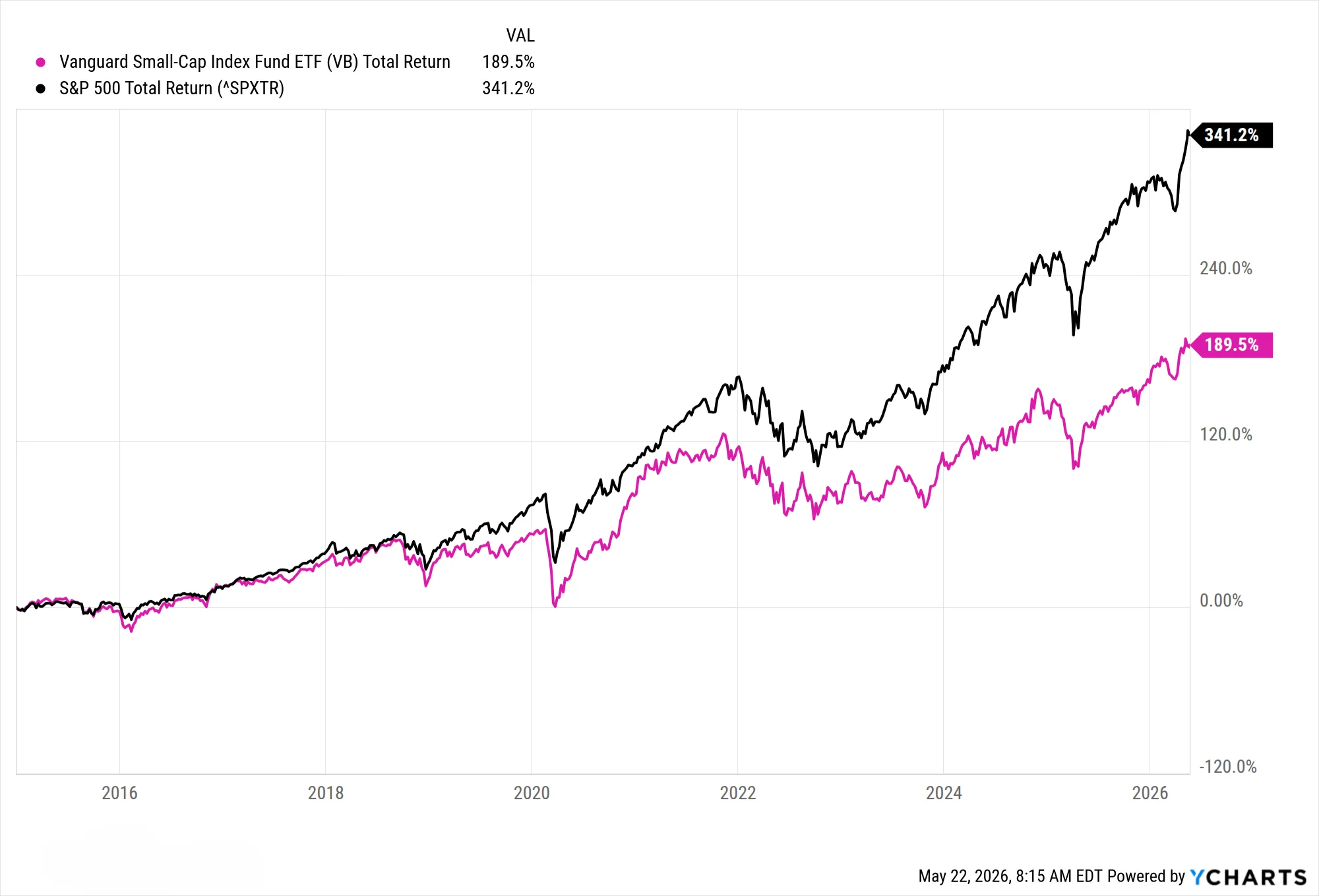

Since 2015, the small-cap index returned 189.5% on a total return basis. The S&P 500 returned 341.2%. That is not a small gap. It is a structural one, and it has been widening, not closing.

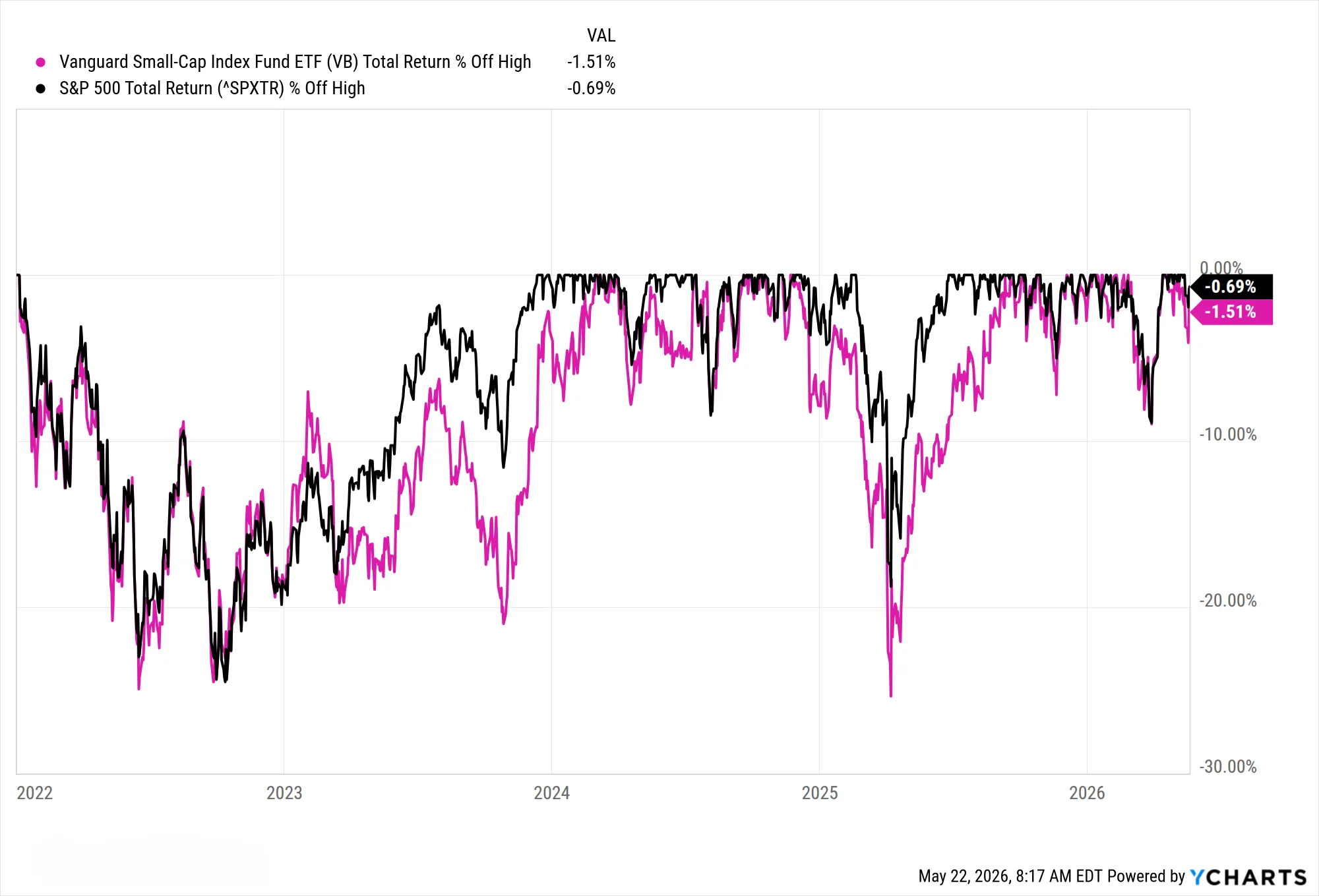

The drawdown picture is worse.

Small caps don’t just underperform on the way up. They fall further on the way down. For a retiree withdrawing income, that combination - lower returns, deeper drawdowns - is the worst possible pairing. It is the math of sequence risk working against you on both sides.

If you are still in your 30s or 40s and accumulating, small-cap exposure delays your retirement. Working longer and saving more can make up for the drag on your portfolio. The same drag appears inside target-date funds: my S&P 500 vs. target-date fund comparison shows how small caps and other added holdings translated into 4.5 to 5.6 additional years to reach $1 million.

If you are in retirement, or near it, the question is different. You are no longer adding capital. You are withdrawing it. Every percentage point of return matters. Every percentage point of drawdown is a withdrawal from a smaller base. There is no second chance to make up the difference.

That is why your retirement income portfolio needs more than a pile of tickers. It needs each asset to do a specific job: growth, stock income, bond income, inflation protection, or downside defense.

For retirees, owning structurally weak businesses isn’t just an academic problem. Lower returns and deeper drawdowns directly increase the odds of running out of money.

The fix isn’t complicated. You don’t need to sell every fund you own. You need to understand what’s inside the ones you do, and eliminate the zombies.

The goal is not owning more tickers. It is owning assets with different jobs. Diversify by function, not ticker. If you need portfolio income, start with a retirement income portfolio built around multiple income sources instead of one fragile bet.

Nobody is watching the dead weight in your portfolio.

Gold+ is your retirement navigation system: find your number, follow the portfolio built for your stage, and get a specific action when market risk changes.

This article is for educational and informational purposes only and does not constitute investment advice. If this article discusses any security, the discussion is for educational purposes only and should not be interpreted as a recommendation, solicitation, or personalized advice. The author may have holdings in the securities discussed. Refined FI is NOT a registered investment advisor. Past performance is not indicative of future results. All investing involves risk, including possible loss of principal. Performance figures sourced from YCharts as of May 22, 2026. Refined FI receives $0 in affiliate revenue, commissions, or compensation from any fund company or financial institution mentioned in this article.

If your portfolio holds small-cap funds, you're carrying dead weight into retirement. The market has changed.

6 min read

The Permanent Portfolio got the framework right: assets need jobs. But one fixed 25/25/25/25 allocation may not solve retirement.

7 min read